Finding the right equipment for your business is a significant achievement. After all, it can act as the backbone of your business value proposition. However, how do you ensure the equipment leasing process is seamless?

Welcome to the comprehensive guide to an equipment rental agreement. This article explores its nuances, types, and best practices for drafting a foolproof equipment lease agreement.

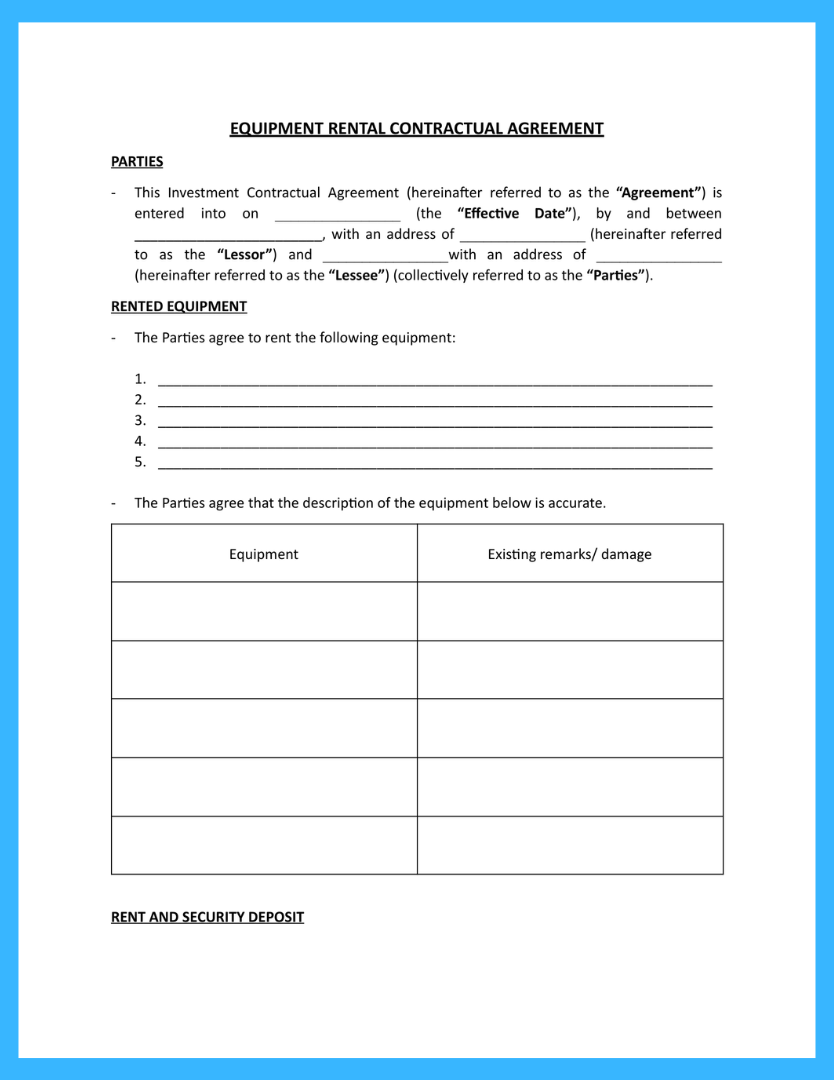

An equipment rental agreement, also known as an equipment lease agreement, is a formal contract between the owner of the equipment (the lessor) and the entity seeking to rent the equipment (the lessee). This lease agreement defines the terms and conditions under which the equipment is rented, safeguarding the rights and obligations of both parties.

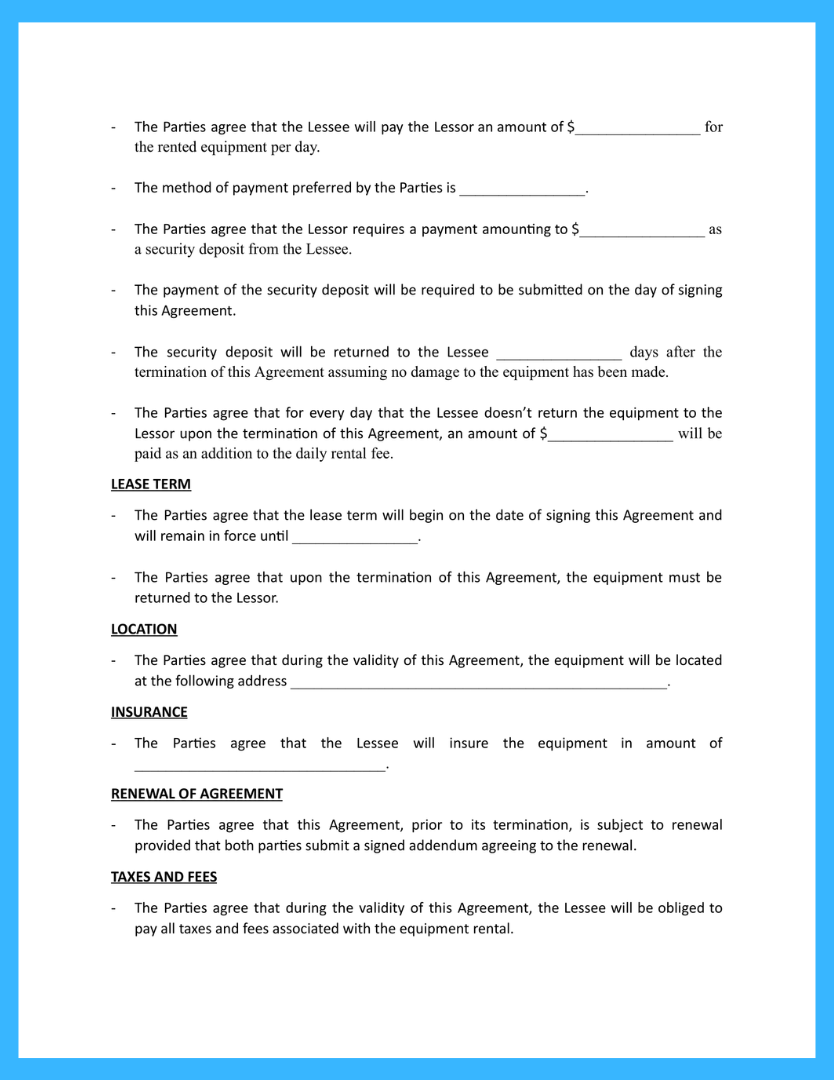

The agreement encompasses critical details like the duration of the lease, rental payment, security deposit, maintenance responsibilities, and insurance requirements. The equipment could be anything from construction machinery , medical apparatus, kitchen equipment, or IT hardware.

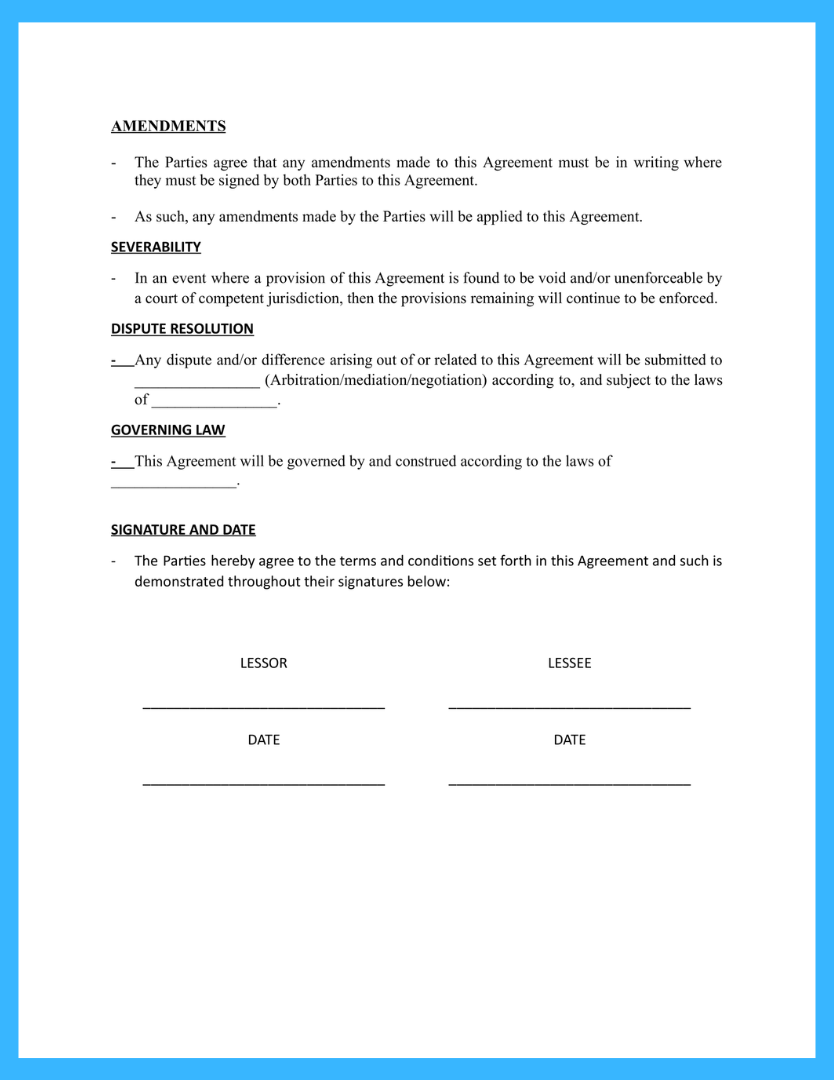

This legally binding rental equipment agreement form ensures clarity between the parties involved, minimizing potential disputes. It’s an essential tool for conducting business, especially in markets where leasing equipment is more cost-effective than purchasing it outright.

Equipment rental agreements vary depending on the industry and the type of equipment being leased. For instance, businesses may lease cranes, excavators, or bulldozers in the construction industry. Restaurants might rent commercial ovens, refrigerators, or espresso machines, while healthcare facilities often lease sophisticated medical equipment like MRI machines or ultrasound devices.

Two primary types of equipment lease agreements include the standard equipment lease and the lease-to-own deal. The standard lease enables businesses to rent equipment for a specified duration, after which the equipment is returned. This model is ideal for companies needing equipment for temporary projects or wanting to avoid the cost of owning, maintaining, and updating the equipment.

On the other hand, a lease-to-own agreement allows the lessee to purchase the equipment at the end of the lease term. This type of agreement can be attractive for businesses looking to acquire equipment without the hefty upfront costs.

DISCLAIMER: We are not lawyers or a law firm and we do not provide legal, business or tax advice. We recommend you consult a lawyer or other appropriate professional before using any templates or agreements from this website.